Text Us

Text Us Call Us

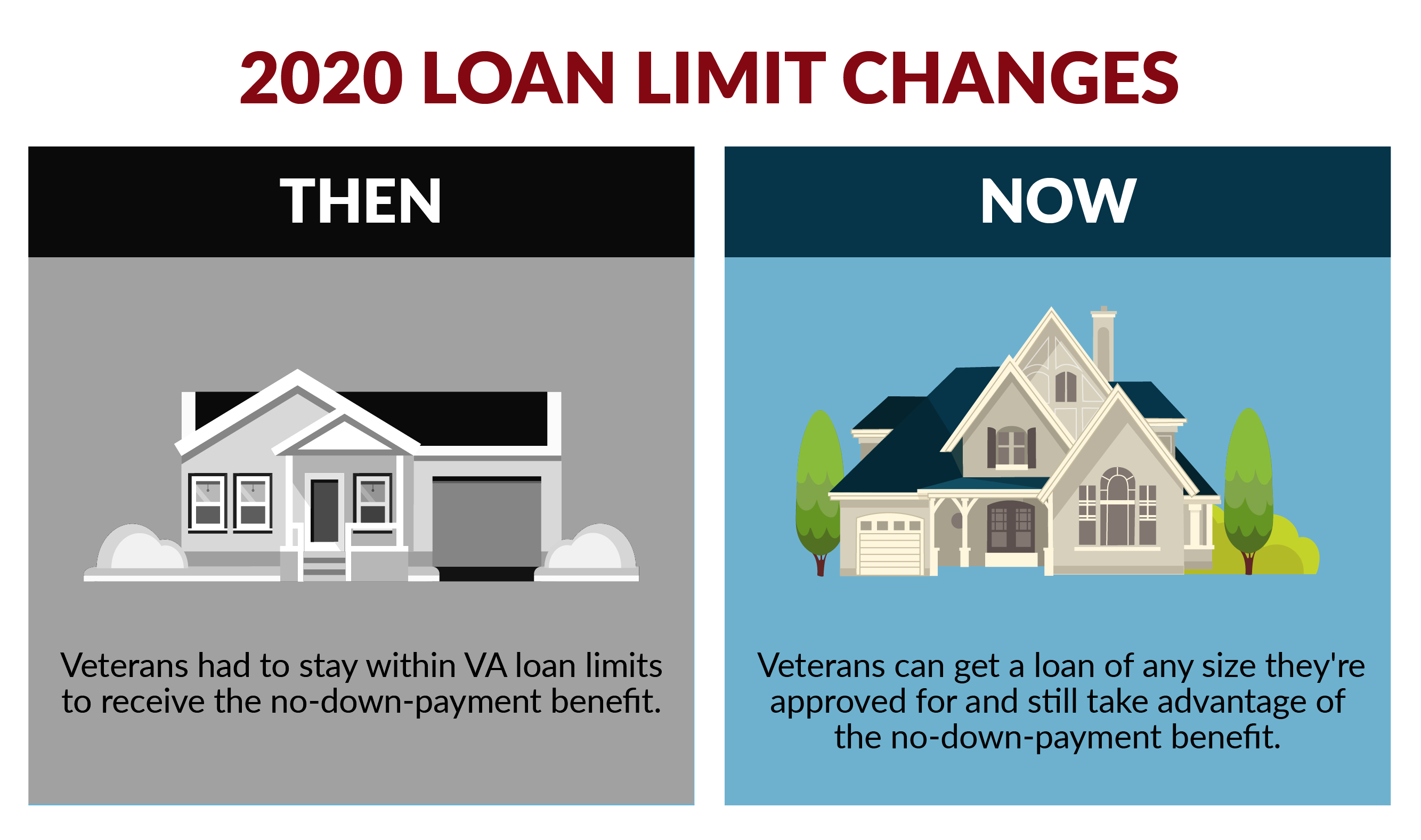

Call UsVA Loan Limits Removed in 2020 with New Law

Sarah Woodbury / Published Nov 22, 2019, 12:16 PM

Sarah Woodbury / Published Nov 22, 2019, 12:16 PM

Vets Can Now Get a Bigger VA Home Loan

Because of the sacrifices they've made serving our country, veterans have the option of using a VA loan on home purchases. This loan type is designed to be a benefit, allowing more servicemembers access to home loans at great rates—and with no down payment.

In 2020, things are even better for veterans looking to get a VA loan. A recent law change means veteran loans no longer have to be within the VA loan limits that were previously required to buy a home without a down payment.

Why the Change to VA Loan Limits?

In the past, some veterans faced a barrier when they tried to get a home using their VA mortgage benefits: VA loan limits.

Prior to 2020, limits on VA loan amounts were based on conforming loan limits set by Fannie Mae and Freddie Mac. For VA loans, they defined the amount the VA could guarantee on a VA loan in each county.

Let's go over just what that means.

The VA, under previous requirements, could guarantee 25% of a loan within the loan limit. So if you wanted to borrow more than the limit permitted, you'd need to make a down payment equal to 25% of the difference between the limit and the loan amount.

Say you wanted a loan for $600,000, but you lived in a county that, like most counties in 2019, had a VA loan limit of $484,350. You'd have two choices:

- Find a less expensive home that falls under the limit and receive the zero down payment requirement benefit.

- Pay 25% of the difference between the loan limit and actual loan amount, or $28,912.50, as a down payment.

This made one of the most important VA loan benefits—getting a loan with $0 down—difficult for some veterans to access.

What Does This Mean for Veterans?

Under the new law, veterans who qualify can get homes at higher amounts, without having to put money down.

This is great news for veterans in more expensive housing markets or those who would like to get a larger loan while still taking advantage of the benefits they've earned.

It's important to keep in mind that veterans still need to be approved by a VA mortgage lender to get a loan.

While the law change makes it easier for veterans to get larger loans because of the opportunity to put 0% down on the home, it won't change the stricter requirements that are often attached to larger mortgages.

Does This Apply to All Veterans?

Veterans must have full VA entitlement to qualify under the new law. If you don't have full entitlement, you'll still be required to get a loan within the loan limits.

You may not have full entitlement if you already have a VA loan or you've defaulted on a loan. A VA loan officer (like one from Low VA Rates) can help you check your entitlement and determine what kind of loan you qualify for.

The Law Behind the Change: Blue Water Navy Vietnam Veterans Act of 2019

The recent change to VA loan limits was part of the Blue Water Navy Vietnam Veterans Act of 2019 (Public Law 116-23), which offered a variety of adjustments to laws regarding veterans, such as the redefining of Agent Orange Exposure in VA disability benefits and the removal of some fee requirements for Purple Heart Recipients.

There was also a temporary change made as part of this law: slight increases to the VA funding fee. This will help fund the benefits offered to veterans exposed to Agent Orange. In 2022, the fee will return to its original amount, until 2029, when the fee will decrease.

You can learn more about these and other changes in this law made by reading our article about 3 Major Updates to the VA Loan Program.