Text Us

Text Us Call Us

Call Us5 Ways to Pay Less in Closing Costs on a VA Loan

Sarah Woodbury / Published Sep 18, 2019, 1:00 PM

Sarah Woodbury / Published Sep 18, 2019, 1:00 PM

If you've started the mortgage process, you probably know that closing costs can be expensive, equaling around 1–5% of the home price. That's why many veterans looking to get a VA loan wonder if there's an option with no closing costs.

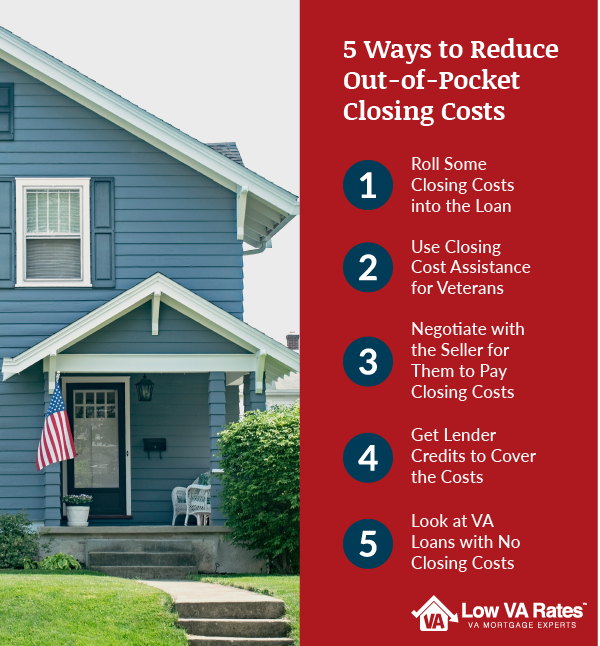

The good news is that there are multiple ways for veterans to lessen or even eliminate VA loan closing costs on their home loan, some of which are listed below:

Keep reading to learn how to make each of these tips a reality for your home loan.

1. Roll Some VA Closing Costs into the Loan

One of the best ways to reduce VA loan closing costs is to roll the VA funding fee into the loan. This fee is typically equal to 1.25–3.3% of the loan amount, so including it in your mortgage can save you a substantial amount at closing.

Most veterans choose to roll the fee into the loan to save on upfront costs, though some do opt to pay it out of pocket.

It's important to keep in mind that rolling any closing costs into the loan will require you to pay more in interest over the long run. This is because you're increasing the loan amount, which in turn increases the amount of interest you'll pay.

However, this option is helpful for those who may not have enough money saved to pay the funding fee upfront or who don't want to spend their savings and would rather include the fee as part of the loan amount.

Here's a simplified example to give you a sense for how costs could change if you included the VA funding fee in your loan.

Let's say you're getting a $200,000 mortgage. You put 5% down and are an active-duty veteran, so your VA funding fee amount is 1.25% of the loan, which equals $3,000.

If you pay the fee upfront, you won't have to pay interest on the fee amount. You'd end up paying $6,500 in interest on the mortgage. In total, you'd pay $209,500 for the mortgage amount, interest, and funding fee over the life of the loan.

However, if you roll the fee into the loan, you'd pay $6,597.50 in interest, which means the total amount you'd pay for the loan would be $209,597.50.

As you can see, the interest added by the VA funding fee isn't much. You'd only pay $97.50 in interest on the fee over the long run.

Essentially, in this example, you'd have to decide whether it's worth paying an additional $97.50 over the life of the loan to avoid paying the $3,000 funding fee upfront.

For many veterans, paying slightly more in interest to avoid the significant upfront cost is worth it. However, the best option for you depends on your individual situation.

2. Use Closing Cost Assistance for Veterans

Depending on your area, there may be programs and grants available to help veterans reach their goal of homeownership.

According to VA loan expert Maurice Navarro, these programs usually vary locally, sometimes differing even between counties. You can visit your local VA office to learn more about what programs are available in your area and for your specific situation.

You can also ask your VA lender if they're aware of any veteran homeownership assistance programs you might be able to apply for. Look for lenders that specialize in VA loans, like us at Low VA Rates, so you're getting information from experts that are more familiar with opportunities available for veterans.

3. Negotiate with the Seller to Have Them Pay Closing Costs

Perhaps one of the best ways to reduce VA closing costs is to ask for the seller to pay for them. As part of the homebuying negotiations, it's perfectly acceptable to ask for any/all costs to be paid by the seller.

The closing costs a seller agrees to pay are called concessions, and they can include the VA funding fee, property taxes and insurance, and other specified costs.

Whether the seller will agree to pay for these costs depends on multiple factors, like how long the home has been on the market or what kind of housing market you're in. If you're in a buyer's market, you'll likely find sellers who are more willing to pay some closing costs.

It's important to know that no seller is required to pay closing costs, but it's still in your best interest to make sure you ask.

Learn more details about seller concessions on VA loans in the video below.

[embed]https://www.youtube.com/watch?v=qs2ktEHyXjw[/embed]

4. Get Lender Credits to Cover the Costs

Another helpful way to reduce upfront costs on a VA loan is to ask your lender for lender credits.

Like with most lender-buyer agreements that lower closing costs, your interest will usually increase with this option. A higher interest rate helps cover the cost your lender is paying for you at closing. It spreads it out over a longer period of time, however, making it more manageable for many borrowers.

Also similar to other closing cost-saving options, you'll want to consider whether the additional money paid in interest over the long run is worth the upfront savings.

5. Explore VA Loans with "No Closing Costs"

If you're looking for a "no closing cost" VA loan, the VA IRRRL is a great option if you already have a VA loan and want to refinance. With the IRRRL, you're able to roll all of the closing costs into the loan.

Similar to what happens when you roll the VA Funding Fee into a loan, this option increases the balance of your loan, but allows you to pay less upfront.

You'll want to remember that there are no true "no closing cost" VA loans, since you'll still need to pay for the costs (plus interest) over the life of the loan.

However, any costs you can roll into the loan will mean you pay less money out-of-pocket on your home purchase, which is especially useful for veterans who can't afford a large upfront payment or would like to keep their money in savings or use it for investments.

Talk to a VA lender to learn about your options for rolling closing costs into your VA loan.

In the meantime, watch Eric Kandell, president of Low VA Rates and VA loan expert, discuss how this works in the video below.